Table of Contents

Enjoying the article?

Don't forget to share with your friends and network to help grow the amazing Gigable community.

In late 2025, the Irish Revenue Commissioners announced a time-limited settlement opportunity for contractor misclassification, allowing businesses to correct genuine classification errors for the 2024 and 2025 tax years before the window closes on 30 January 2026. (Crowe, 2025)

This announcement followed the landmark Supreme Court decision in Revenue Commissioners v Karshan (Midlands) Ltd t/a Domino’s Pizza, which clarified how employment status should be assessed for tax purposes in Ireland.

For businesses that rely on contractors or freelancers such as delivery drivers, this is not just a legal update. It is a practical moment to review how workers are engaged, managed, tracked & paid in reality, and to decide how compliance should be handled going into 2026 and beyond.

Many businesses are now looking for more effective ways to manage contractor compliance, ensuring they can assess risk accurately and avoid potential penalties.

Revenue’s settlement window provides businesses with an opportunity to make a voluntary disclosure where workers may have been incorrectly classified as contractors rather than employees, without penalties, interest, or publication, provided the misclassification arose from a bona-fide error and disclosure is made before 30 January 2026.

Revenue has acknowledged that many businesses relied on earlier guidance in good faith, and that the Karshan judgment materially changed how employment status must be assessed. The settlement window exists to allow businesses to regularise their position under this updated framework.

However, the settlement applies only to past periods (2024–2025). The expectations around compliance, documentation, and evidence apply fully going forward.

A central takeaway from the Karshan / Domino’s decision, and from Revenue’s subsequent guidance, is that:

|The reality of the working relationship matters more than the existence or content of any contract.

In practice, the level of control exercised by the business is often the primary driver when determining worker classification. Revenue and the courts look closely at who controls how, when, and where the work is carried out, regardless of how the relationship is described on paper.

That assessment is then reinforced by other key factors, including:

In the Domino’s case, delivery drivers were classified as employees for tax purposes because the factual working arrangements pointed toward employment, regardless of contractual labels.

This principle underpins Revenue’s current approach to contractor compliance.

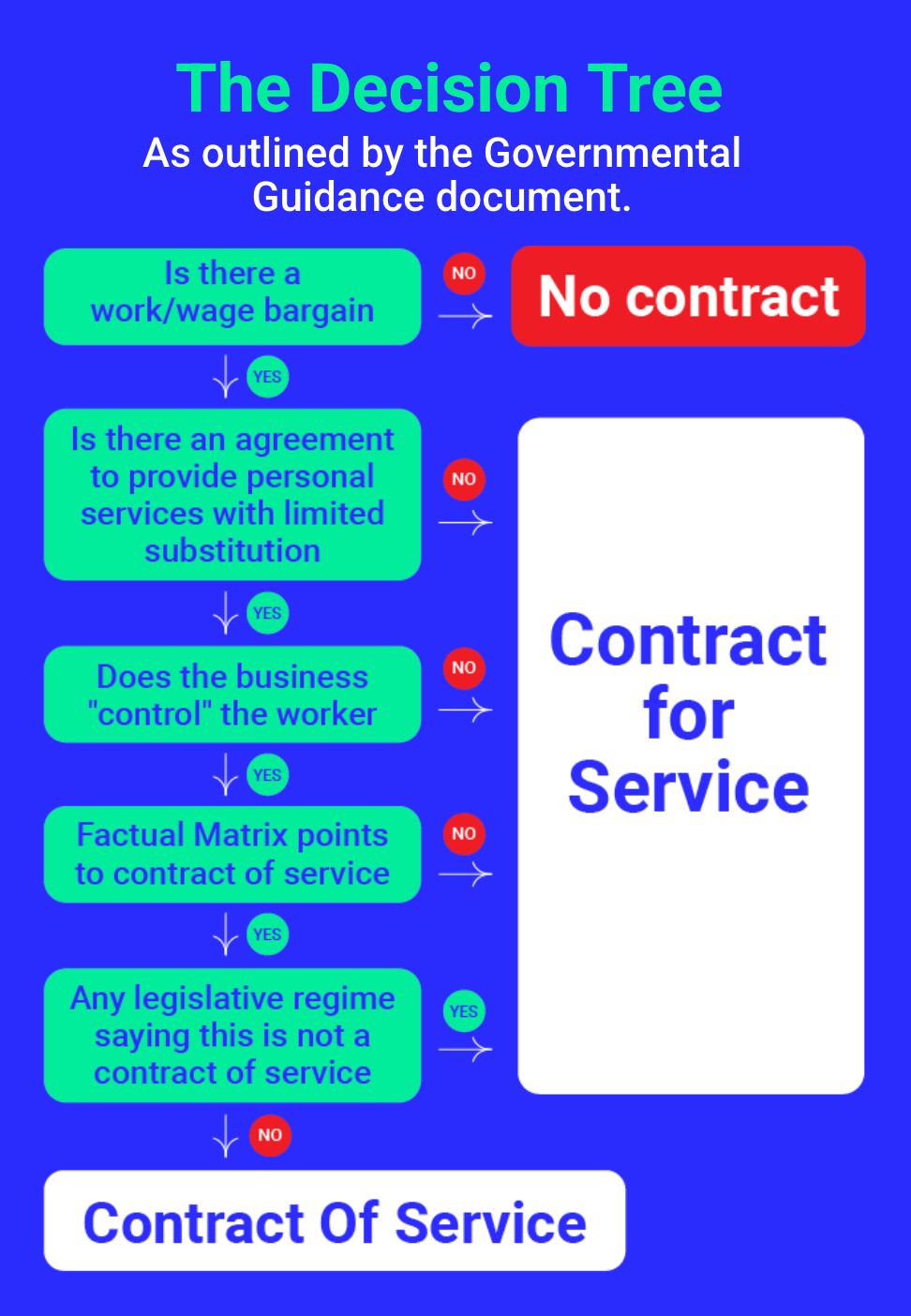

Revenue and the courts apply the five-point criteria, as outlined in recent governmental guidance following the Karshan decision. (Revenue, 2025)

This framework reinforces that employment status is determined by how the relationship operates in practice, not by labels or intent alone.

And the decision tree below summarises the framework set out in governmental guidance and Supreme Court case law. While not a substitute for professional advice, it illustrates the logic Revenue applies when assessing employment status.

For businesses, the implication is clear:

you must be able to evidence how work is performed, tracked, and paid.

Contractor misclassification rarely arises from deliberate action. More often, it develops gradually as businesses grow and operations evolve.

Common challenges include:

Individually, these processes may function well. Collectively, they can make it difficult to demonstrate compliance when required. This is where a workforce compliance solution becomes increasingly important, helping businesses maintain consistent, audit-ready records across teams and locations. For businesses operating in sectors like delivery and hospitality, where teams are distributed and operations move quickly, these challenges become even more pronounced.

As operations scale, businesses need a contractor management platform to track classification, documentation, and audit readiness efficiently.

While the Revenue settlement window closes on 30 January 2026, the underlying compliance expectations do not.

Many businesses are using this period to adopt a smarter strategy putting systems in place so that evidence Revenue expects is created automatically as part of daily operations.

In practical terms, this means:

To mitigate these risks, businesses should adopt a compliance management solution that centralises contractor data and ensures ongoing regulatory alignment.

This is where Gigable CMS (Contractor Management Software) supports businesses operationally with compliance management built in from day one.

Gigable does not provide legal or tax advice. Instead, it helps businesses operate compliantly in practice by:

By embedding compliance into everyday operations rather than a separate task, businesses reduce risk, avoid disruption, and enter 2026 with greater confidence.

If you’re looking for a calmer, more joined-up way to manage contractors in 2026, you can explore how Gigable CMS works here.

Take the next step and join Gigable today. Let's put those insights into action and boost your business or freelance career!